“The CFPB is proposing clear, enforceable rules that will reduce overdraft fees and save Americans billions, closing another lucrative regulatory loophole banks use to prey on consumers,” said one advocate.

Consumer Financial Protection Bureau Director Rohit Chopra testified on a semi-annual report of his agency before the House Financial Services Committee on Nov 29, 2023. Screenshot: C-SPAN

In a move cheered by progressive advocates, the U.S. Consumer Financial Protection Bureau on Wednesday proposed a new rule limiting how the nation’s biggest banks can charge overdraft fees.

The CFPB said its proposal “would close an outdated loophole that exempts overdraft lending services from long-standing provisions of the Truth in Lending Act and other consumer financial protection laws.”

Day of Action artbuild in North Carolina. Photo: Third Act/Twitter

Determined not to leave all the responsibility for climate action with young campaigners like Greta Thunberg and the Sunrise Movement, older Americans are organizing a nationwide Day of Action planned for Tuesday, with the aim of wielding the relative political and economic power of people aged 60 and up to pressure big banks to stop funding fossil fuel projects.

Following actor and activist Jane Fonda’s “Fire Drill Friday” protests that began in Washington, D.C. in 2019, longtime climate advocate Bill McKibben founded Third Act last year to mobilize older Americans who wanted to show solidarity with the Generation Z activists leading worldwide climate protests in recent years. Continue reading →

“Investors are saying we can’t conduct business in a world that is on fire, that has heatwaves and insufficient water. And I do think companies are beginning to understand that it’s in their interest to take action.”

Protest outside the Bank of America shareholder meeting on April 25, 2022. Photo: drew hudson #1u/Twitter

A significant percentage of shareholders at three of the biggest U.S. banks voted Tuesday to endorse first-of-their-kind resolutions urging the companies to stop supporting new fossil fuel development amid a worsening climate emergency.

Shareholders at Citi, Bank of America, and Wells Fargo voted 12.8%, 11%, and 11%, respectively, to support climate resolutions filed by the Sierra Club Foundation and other members of the Interfaith Center on Corporate Responsibility. According to the Sierra Club, any resolution that receives at least 5% of the vote can be refiled the following year, and those that get 10% or more are “considered difficult for a company to ignore.” Continue reading →

“This is the way things work when democracy has been weakened,” argued one progressive organization. “The powerful get special access to our government, while we’re told, ‘Sorry, we can’t help you.'”

New federal disclosures reveal that major corporations poured donations into West Virginia Sen. Joe Manchin’s political action committee in the weeks leading up to his pivotal announcement Sunday that he would oppose the Build Back Better Act, a stance that progressives argue is motivated by the senator’s deference to special interests.

CNBCreported late Tuesday that Federal Election Commission (FEC) filings show that donors to Manchin’s Country Roads PAC raked in 17 contributions from corporations in October and 19 in November as he pared back and repeatedly threatened to tank Democrats’ $1.75 trillion social spending and climate legislation. Continue reading →

The Bank Policy Institute, a lobbying group for big banks, drew criticism for a policy memo suggesting financial deregulation as a response to the coronavirus outbreak. (Photo: Phillipp/Flickr/cc)

A lobbying group for big banks in the United States came under fire Tuesday from financial industry experts for pressuring federal officials to push through long-sought regulatory rollbacks in response to the worldwide economic concerns sparked by the global coronavirus outbreak.

On Sunday, Bank Policy Institute (BPI) chief executive Greg Baer, head of research Francisco Covas, and chief economist Bill Nelson published a post on the group’s website entitled “Actions the Fed Could Take in Response to COVID-19.” The BPI is a lobbying group whose members include Bank of America, Citigroup JPMorgan Chase, and Wells Fargo. Continue reading →

Apparently not satisfied with access to its users’ call history, text messaging data, and online conversations, Facebook has reportedly asked major Wall Street firms like JPMorgan Chase and Wells Fargo to hand over their customers’ sensitive financial data as part of the social media giant’s ongoing attempt to become “a platform where people buy and sell goods and services.”

And according to the Wall Street Journal—which first reported on Facebook’s plans on Monday—the social media behemoth isn’t the only tech company that wants access to Americans’ financial data. Google and Amazon have also “asked banks to share data if they join with them, in order to provide basic banking services on applications such as Google Assistant and Alexa,” the Journal pointed out, citing anonymous sources familiar with the companies’ ambitions. Continue reading →

The new report “names those that are still okay with trying to make a profit from producing nuclear weapons.” (Photo: ippnw Deutschland/flickr/cc)

A new report offers a comprehensive look at who’s profiting from the new nuclear arms race.

“If you have been wondering who benefits from Donald Trump’s threats of nuclear war, this report has that answer,” said Beatrice Fihn, executive director of the International Campaign to Abolish Nuclear Weapons (ICAN), winner of the 2017 Nobel Peace Prize.

ICAN, along with Netherlands-based peace group Pax, released the report, entitled “Don’t Bank on the Bomb,” on Wednesday. It shows that 329 financial institutions in 24 countries invested $525 billion into the top 20 companies involved in the production, maintenance, and modernization of nuclear weapons from January 2014 through October 2017. Continue reading →

President Donald Trump has been waging a war on regulation since he got into office on the ground that government red tape costs the economy billions of dollars a year.

Among the victors in this battle have been energy companies, banks and the president himself, who recently promised he’s “just getting started.” Perhaps the biggest losers, however, have been consumers.

The agency was launched in 2011 in the aftermath of the financial crisis as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The goal was to protect consumers from deceptive or misleading practices in the financial industry.

At the moment, Republicans seem focused on blocking CFPB rules they don’t like, such as one that would have prevented the use of arbitration clauses in financial contracts, making it easier for people to band together to sue banks for wrongdoing. Separately, the Trump administration has been heavily critical of the CFPB, and its director is said to be considering leaving before his term expires next July, which would allow the president to pick his replacement.

So what would you miss if the agency suddenly disappeared or got gutted?

In short, a lot. We base this conclusion on the work the three of us have done in recent decades. One of us (Sovern) has been writing about consumer law for more than 30 years, while the other two of us direct a legal clinic that represents elderly consumers. We’ve seen the worst of what financial companies can do, and we’ve also witnessed how the CFPB has begun to reverse the tide.

John Stumpf, far left, lost his job as CEO of Wells Fargo as a result of the scandal over fraudulent accounts.Reuters/Gary Cameron

Life before CFPB

If you are one of the more than 29 million consumers who have collectively received nearly US$12 billion back from misbehaving financial institutions because of the CFPB’s efforts, you already know its value. But even if you are not, you have probably benefited from the bureau’s existence.

Before Congress created the bureau, there was no federal agency that made consumer financial protection its sole mission. Rather, consumer protection was rolled into the missions of a bunch of different agencies. And, as we saw during the financial crisis, regulators often gave it a back seat.

Congress, for example, gave the Federal Reserve the power to bar unfair and deceptive mortgage lending in 1994. Yet the central bank considered consumer protection a backwater and didn’t use that power until 2008 – too late to prevent the Great Recession. Congress took it away two years later when it passed Dodd-Frank.

The Office of the Comptroller of the Currency regulates banks but was so preoccupied with ensuring lenders were safe that it failed to protect consumers from their predatory subprime mortgages – so much so that it prevented states from doing so too. And now President Trump has put a former bank lawyer in charge of it. The Federal Trade Commission, which is tasked with fighting deceptive business practices, lacked the power to prevent such dangerous lending.

This meant consumer protection on financial matters fell through the cracks.

But as early as 2010, before the CFPB was set up, regulators at the OCC were increasingly aware of what was happening at Wells Fargo thanks to hundreds of whistleblower complaints. The OCC even confronted the bank, yet failed to take any action despite many red flags, according to an internal audit.

When the bureau began publishing consumer complaints on its website, companies that might previously have ignored negative feedback paid attention. Financial institutions have responded to complaints to the CFPB more than 700,000 times, often by providing a remedy to the consumers.

Besides protecting consumers, however, Congress had a second motive in creating the bureau: to help prevent the kind of mortgage lending that helped cause the Great Recession.

To that end, the bureau has adopted rules that help consumers to understand their mortgages – something that often wasn’t possible under the previously misleading mortgage disclosures. It also issued regulations to prevent consumers from taking out mortgages that they couldn’t repay. And after borrowers take out a mortgage, CFPB servicing rules establish the procedures servicers must follow when communicating with borrowers, correcting errors, providing information and dealing with loan modification requests.

Two of us have personal experience with one of the bureau’s new mortgage rules, which powerfully illustrates the value of the CFPB.

In 2014, Alice, a client of our law school clinic, was struggling to pay the mortgage on her home – which she had refinanced a few years earlier – after a stroke forced her into retirement. Our clinic helped her apply for a modification of her loan.

But within weeks, instead of acknowledging Alice’s application, the loan servicer summoned her to court to begin foreclosure proceedings in violation of CFPB servicing rules. Fortunately, our clinic was able to rely on those rules in getting the foreclosure action dismissed. Alice got her loan modified and remains in her home.

Demonstrators tried to draw attention to the subprime mortgage crisis back in early 2008.AP Photo/Matt Rourke

Protecting the vulnerable

This reveals how the bureau is particularly important to protect vulnerable consumers, like the elderly, who are frequently targeted by fraudsters and predatory lenders because of their cognitive and other impairments and because they often have accumulated substantial assets. The CFPB is the only federal agency with an office specifically dedicated to protecting the financial well-being of older adults.

Given Alice’s ill health, the consequences for her might have been disastrous if she had been thrown out of her home. But now she – and all of us – face the loss of the CFPB’s aid.

The House of Representatives has passed a bill that would cripple the CFPB by, for example, taking away the power it used to fine Wells Fargo for opening illegal accounts and concealing its complaint database from public view. In other words, it would force the bureau to sit idly by as financial institutions lie to consumers. Even if the bureau survives, it may be less protective of consumers when its current director, Richard Cordray, leaves. His term expires next summer, and he may step down even sooner. Then we might see a former banker or bank lawyer put in charge, just as has happened at the Treasury Department and comptroller’s office.

Nearly every American has or will have a loan or bank account, a prepaid card, credit card, a credit report or some combination of those, and so has dealings with a financial institution policed by the CFPB. But few of us read the fine print governing these things or can understand it when we do. That gives the companies that write these agreements the ability to draft them to suit their own interests at the expense of consumers.

Similarly, we do not always know when a financial institution takes advantage of us, just as Wells Fargo customers did not always know that it had opened unauthorized accounts that lowered their credit scores.

Consumers need protection from misbehaving companies. If the bureau is eliminated, significantly weakened or starts protecting banks rather than consumers, all consumers will suffer.

This is an updated version of an article originally published on July 10, 2017.

About the Authors:

Jeff Sovern, Professor of Law, St. John’s University

Ann L. Goldweber, Professor of Clinical Education, St. John’s University

Gina M. Calabrese, Professor of Clinical Education, St. John’s University

Disclosure statement

Along with three co-authors, Jeff Sovern received a $29,510 grant from the American Association for Justice Robert L. Habush Endowment and by a grant from the St. John’s University School of Law Hugh L. Carey Center for Dispute Resolution in 2014 to study arbitration. It resulted in an article. Along with Professor Kate Walton, he received a grant from the National Conference of Bankruptcy Judges Endowment for Education to study debt collection, resulting in another article. He is a member of the National Association of Consumer Advocates.

Ann L. Goldweber is affiliated with NACA as a member.

Gina M. Calabrese is affiliated with the National Association of Consumer Advocates, New Yorkers for Responsible Lending, and the Association of the Bar of the City of New York (former chair, Committee on the Civil Court).

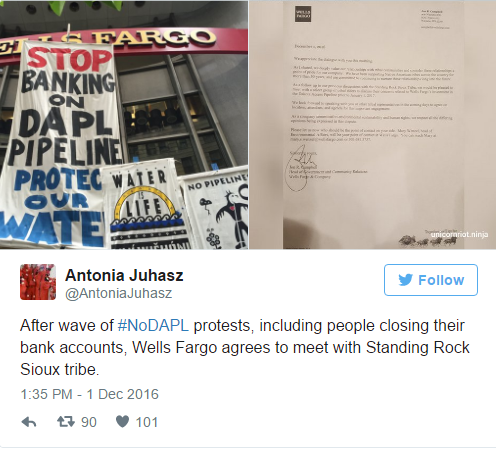

Global demonstrations are calling on banks to divest from the controversial Dakota Access Pipeline, citing human rights abuses against water protectors

The Bank of Tokyo-Mitsubishi UFJ, Mizuho Bank, Sumitomo Mitsui Banking Corporation and SMBC Nikko Securities Inc. are all involved in the Dakota Access Pipeline, and activists in Tokyo demanded the financiers divest. (Photo: 350.org Japan)

Update:

Organizers report that after the series of demonstrations on Thursday, Wells Fargo—a Dakota Access Pipeline investor—has agreed to meet with the Standing Rock Sioux Tribe: